Legal structure

Overview¶

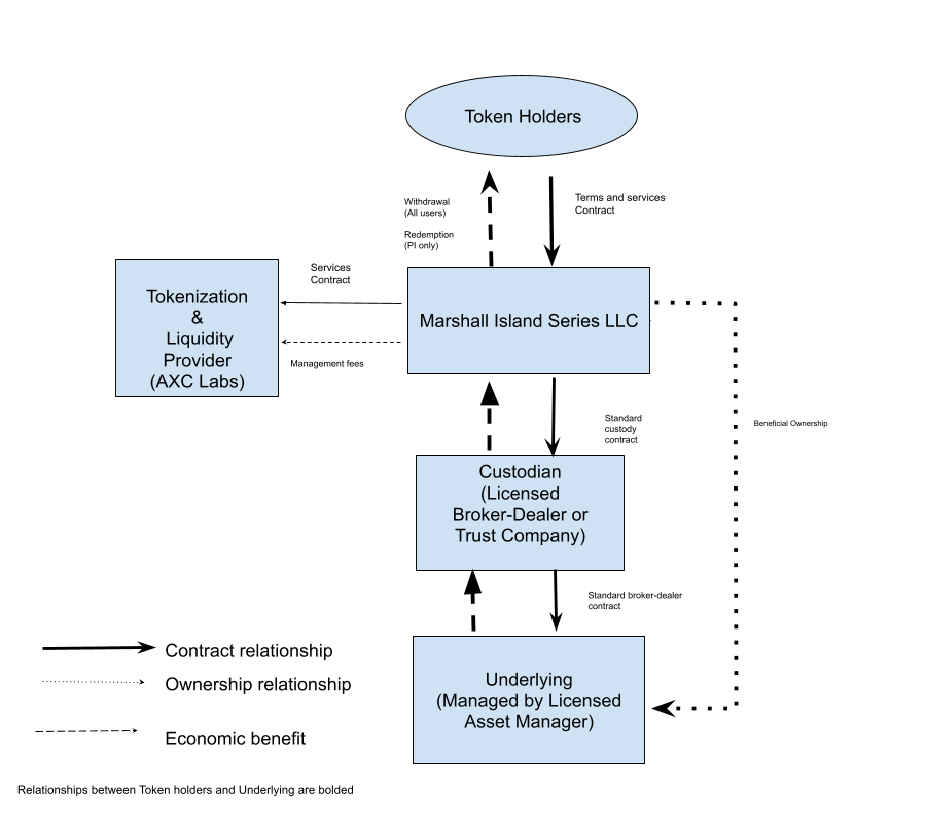

The legal architecture is designed to grant permissionless token holders direct economic exposure to the returns of the underlying assets, as well as access to the value of the assets in the event of liquidation, while maintaining regulatory compliance and institutional-grade bankruptcy remoteness all while minimizing regulatory friction.

The basic legal and entity architecture of the AXC permissionless token (distributed asset) is as follows:

To achieve the goals of transferability, financial privacy, and regulatory compliance for permissionless tokens, the protocol utilizes a Master/Series DAO LLC structure. Shares of the underlying asset are purchased from an asset manager and beneficially owned by a specific Series DAO LLC, which operates under a Master DAO LLC.

For example, in the case of the permissionless Growth Yield Token, the Master DAO is RWAfi DAO LLC (a Marshall Islands non-profit entity filed with a single member). The Series DAO (RWAfi DAO LLC - Series 1) holds the assets and issues the ERC-20 tokens. AXC acts strictly as the technology provider, and receives a management fee for operating the token-related platform.

| Actor | Legal Domicile | Role |

|---|---|---|

| Master/Series DAO LLC (e.g. RWAfi DAO LLC / RWAfi DAO LLC - Series 1) | Marshall Islands | Master sets up Series LLC’s to hold assets and has direct relationship with custodian Series has beneficial ownership of underlying asset |

| Blockchain Service Provider (e.g. AXC) | Caymans | Provides technical support in connection with issuance and management of tokens - receives management fee |

| Underlying manager | Various | Asset manager |

| Custodian | Hong Kong | Trust relationship to hold cash and the underlying asset on behalf of the token issuer. |

Governing Legal Agreements¶

For the permissionless tokens, the relationships between the entities, the service providers, and the token holders are governed by a framework of legal contracts:

| Contract | Parties | Description |

|---|---|---|

| Terms and conditions contract | Token holders and Series LLC | Governs obligations to tokenholders |

| Token memorandum | Token holders and Series LLC | Governs use of funds for the token |

| Custody/Ownership contract | Master LLC and Series LLC | Permits Master LLC to act on behalf of Series |

| Blockchain services Contract | Series LLC and Blockchain service provider | Permits the Blockchain service provider to provide services to Series LLC |

| Custodial account | Master LLC and Custodian | Trust account agreement |

Terms and Conditions (Token Holders & Series LLC)¶

Governs the primary obligations to token holders. It emphasizes the non-custodial token structure, clarifies that tokens do not represent equity or ownership rights in the LLC or the underlying asset, and outlines broad jurisdictional transfer restrictions, and limits issuer liability. Disputes are governed by Marshall Islands law and HKIAC arbitration.

Token Memorandum (Token Holders & Series LLC)¶

Details the mechanics of the ERC-20 token. It specifies that the token economically tracks the fund via the issuer holding its shares, allowing only indirect participation. It also highlights potential tracking errors due to liquidity and fee management, alongside standard market and underlying-asset risks.

Custody/Ownership Contract (Master LLC & Series LLC)¶

Permits the Master LLC to act on behalf of the Series LLC, and specifies that all series assets (cash, tokens, underlying securities) are beneficially owned by the specific Series, even if legally titled under the Master LLC. This architecture is intended to create asset segregation so that the assets held for one town cannot be used to satisfy other series or master-level liabilities.

Blockchain Services Contract (Series LLC & AXC)¶

Appoints a non‑fiduciary token services provider on a non‑exclusive basis, sets flexible fee mechanics (including unilateral changes with a termination right), heavily limits liability except for negligence or fraud, defines force majeure and creates a HKIAC arbitration framework under Marshall Islands/Delaware‑reference law.

Custodial Account Agreement (Master LLC & Custodian)¶

Establishes a Hong Kong institutional/professional investor securities account. It includes product risk disclosures and grants the licensed broker the right to suspend the account or request information in compliance with AML/KYC regulations.

Structural Protections & Risk Mitigation:¶

Special Purpose Vehicle (SPV) Structure¶

Each individual fund is siloed into a separate Marshall Islands Series LLC. This SPV contains only the specific underlying assets and holds no external contracts other than those with token holders, the custodian, and essential service providers. To minimize legal risks associated with the recognition of the master/series structure across jurisdictions, all series holdings execute long-only strategies.

Bankruptcy Remoteness & Segregation¶

The legal architecture is explicitly designed to be bankruptcy remote:

Service Provider Isolation: The SPV is legally separated from AXC (the Blockchain service provider). Claims against AXC will not attach to the assets held within the SPV.

Cross-Liability Protection: Each fund maintains a separate balance sheet under Marshall Islands law. Because the funds are long-only, potential token holder claims cannot exceed the assets available in that specific series. To protect against the risk of cross-jurisdictional non-recognition of the master-series structure, if future funds employ strategies with potential excess liability, a completely separate Master DAO LLC will be set up.

Custodian Remoteness: Beneficial ownership of all assets remains with the SPV. Custodians are licensed trust businesses, ensuring that SPV assets are legally segregated from the custodian’s corporate holdings.

Liquidation Rights¶

While the tokens do not grant direct equity ownership or voting rights in the underlying fund, both the General Terms and Conditions and the Investor Addendum state that token holders are entitled to a pro-rata share of the assets held by the SPV in the event of an SPV liquidation.

KYC/AML policies¶

Wallet Screening¶

All on-chain wallets must pass BlockSec’s Phalcon compliance KYT and KYA checks before being approved to hold and receive tokens. This process involves screening wallet addresses and transactions against OFAC sanctions lists, filtering high-risk entities, flagging suspicious flows, and ensuring that every issue is resolved efficiently, with regulator-ready Suspicious Transaction Reports (STRs) available for export.

https://

Jurisdiction Restrictions¶

All users from the United States, Mainland China, and jurisdictions under United Nations sanctions are prohibited from interacting with the AXC protocol. The AXC protocol has also geo-blocked IP addresses from these regions.